Medicare Levy Surcharge 2026: The New Income Thresholds

- Arthur Sterling - Head of Tax Education

- May 5

- 6 min read

Updated: May 29

Quick Answer: The 2025–26 MLS Snapshot

The Medicare Levy Surcharge (MLS) is an extra tax (on top of the standard 2% Medicare Levy) paid by Australians who earn over a certain amount and do not have appropriate private hospital cover. For the 2025–26 financial year, the thresholds have increased:

Income Tier | Single Income | Family Income* | MLS Rate |

Base Tier | $101,000 or less | $202,000 or less | 0% |

Tier 1 | $101,001 – $118,000 | $202,001 – $236,000 | 1.0% |

Tier 2 | $118,001 – $158,000 | $236,001 – $316,000 | 1.25% |

Tier 3 | $158,001 or more | $316,001 or more | 1.5% |

*Note: The family threshold increases by $1,500 for each dependent child after the first.

Introduction: The "Hidden" Tax of Success

In Australia, earning more money is usually a cause for celebration. However, as your career progresses, you hit specific "invisible" lines in the tax code that can trigger unexpected costs. One of the most significant—and often misunderstood—is the Medicare Levy Surcharge (MLS).

As we move through 2026, many Australians have seen their incomes rise due to the recent Stage 3 tax cuts and cost-of-living adjustments. While your weekly take-home pay might look better, these increases could be pushing you into a surcharge tier that costs you thousands of dollars at tax time and if you're in the mid-income range, make sure you also read our guide on the cost of living tax offset 2026 – income thresholds explained to see what relief you may be entitled to at the same time.

At Tax Falcon, we believe you shouldn't be penalised for doing well. This comprehensive guide breaks down the new 2026 thresholds, explains the difference between the "Levy" and the "Surcharge," and shows you how our 10-minute expert review can help you navigate the private health maze to keep more of your hard-earned money.

1. Medicare Levy vs. Medicare Levy Surcharge: What's the Difference?

One of the biggest sources of confusion we see at Tax Falcon is the difference between these two items.

The Medicare Levy (2.0%)

This is a standard tax that almost all Australian taxpayers pay. It helps fund the public health system (Medicare). It is generally 2% of your taxable income. If you earn $90,000, you pay $1,800. There are reductions for low-income earners, but for most people, this is a "set and forget" part of your tax return.

The Medicare Levy Surcharge (1.0% to 1.5%)

The Surcharge is an additional tax. It was introduced by the government to encourage higher-income earners to take out private hospital insurance, thereby reducing the pressure on the public hospital system.

You only pay the Surcharge if you earn over the thresholds listed above AND you do not have the right level of private hospital cover.

If you earn $110,000 (Tier 1) and don't have hospital cover, you pay the 2% Levy PLUS a 1% Surcharge. That’s a total of 3% in health-related taxes.

2. Defining "Income for MLS Purposes"

This is the "gotcha" moment of the 2026 tax season. The ATO doesn't just look at your "Taxable Income" to decide if you pay the surcharge. They use a broader definition called Income for MLS Purposes.

What’s included?

Taxable Income: Your salary, wages, and business profits.

Reportable Fringe Benefits: Any perks from your job (like a car or school fees) that appear on your Income Statement.

Reportable Superannuation Contributions: Any extra super you or your employer put in (above the 11.5% mandatory rate).

Net Investment Losses: If you lost money on a rental property or shares (Negative Gearing), the ATO "adds that loss back" to your income for this calculation.

The Falcon Warning: Many people think they are safe because their taxable income is $95,000. But if they have $10,000 in negative gearing losses and $5,000 in reportable super, their "Income for MLS Purposes" is actually $110,000—placing them firmly in Tier 1.

3. The "Appropriate Level of Cover" Requirement

To avoid the surcharge, you can't just buy any cheap health insurance. The ATO is very specific about what counts as "Appropriate Level of Cover."

Hospital Cover is a Must: You must have private Hospital Cover. An "Extras-only" policy (for dental, optical, or physio) will NOT exempt you from the MLS.

The Excess Limit: For the 2025–26 year, your policy must have an excess of:

$750 or less for singles.

$1,500 or less for families/couples.

If your excess is higher than this, the ATO will still charge you the surcharge as if you had no insurance at all!

4. The "1-Day" Calculation Rule

The MLS is calculated on a daily basis. If you had appropriate hospital cover for 200 days of the year but were uninsured for the other 165 days, you will pay the surcharge for those 165 days.

Strategy for 2026: If you haven't taken out cover yet and you're approaching the threshold, getting covered today won't wipe out the surcharge for the first half of the year, but it will stop the "bleeding" for the remaining months. For other high-impact moves you can still make before the financial year closes, see our guide on the top 5 tax tips before June 30 to maximise your refund.

5. The Private Health Insurance Rebate (The Flip Side)

While the Surcharge is the "stick," the Private Health Insurance Rebate is the "carrot." Depending on your income tier, the government may pay for a portion of your premiums.

In 2026, the rebate rates are adjusted twice a year (April and July).

Base Tier: You get the maximum rebate (approx. 24%).

Tier 3: You get 0% rebate.

When you lodge with Tax Falcon, we cross-reference your income against your health insurance premiums. If you didn't claim your rebate as a discount on your monthly bills, we ensure you get it back as a lump sum in your tax refund.

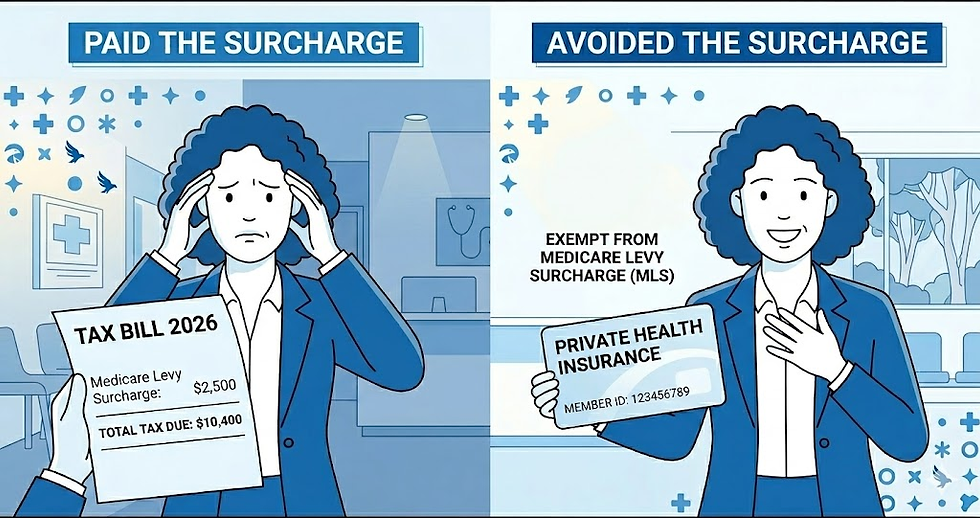

6. Case Study: The "Break-Even" Point

Meet Michael. He’s a software dev earning $115,000 in 2026. He has no dependants and no private hospital cover.

Scenario A (No Insurance): Michael pays 1% MLS. Cost: $1,150.

Scenario B (Basic Hospital Cover): Michael finds a basic hospital policy for $950 a year.

The Result: By spending $950 on insurance, Michael avoids the $1,150 tax. He is $200 better off, plus he actually has the benefit of private hospital access if he needs it.

Falcon Tip: If you are in Tier 1 or higher, private hospital cover is almost always "cheaper" than paying the tax. It’s the rare case where the government literally gives you a reason to buy a service for your own benefit.

7. How Tax Falcon Handles the Surcharge

We know that the Medicare Levy Surcharge is one of the most stressful parts of a high-earner's return. If you're still deciding how to lodge, our comparison of Tax Falcon vs myTax – which is better for you shows exactly why having an expert handle this calculation matters. Our 10-minute online flow is designed to eliminate the guesswork.

Automatic Pre-fill Sync

We pull your private health insurance data directly from the ATO. If your health fund has reported your cover dates and your "share" of the policy, we import it instantly.

The "Surcharge Optimiser"

Our system calculates your "Income for MLS Purposes" (including those tricky super and investment add-backs). If we see you’re on the edge of a tier, we provide clear explanations so you know exactly why your refund looks the way it does.

Expert Review of Dependants

For families, the definition of a "dependant" can be confusing. Does your 22-year-old student child count? Our human experts review your family structure to ensure you are getting the correct $1,500 threshold increase for every child, potentially saving you from a higher tier.

FAQ: Medicare Levy Surcharge Threshold 2026

What if I earn over $101,000 but I'm an international resident?

If you are not eligible for Medicare (e.g., you are on a specific temporary visa and have a "Medicare Entitlement Statement"), you might be exempt from the 2% Levy and the Surcharge. Tax Falcon has a specialized flow for "Medicare Exemptions."

My spouse has insurance but I don't. Do we pay?

For the MLS, the ATO looks at the family unit. If you are a couple and only one person is covered, both may still have to pay the surcharge if your combined income is over $202,000. To be exempt, the entire family (including children) must be covered.

Can I claim my health insurance premiums as a deduction?

No. Private health insurance premiums are not a tax deduction. They only provide you with a "Rebate" or help you avoid the "Surcharge."

Does "Extras" cover help at all for tax?

No. While Extras are great for your teeth and eyes, they have zero impact on the Medicare Levy Surcharge. You must have "Hospital" cover.

Conclusion: Don't Let Your Pay Rise Become a Pay Cut

As you move into the Tier 1 or Tier 2 income brackets in 2026, the Medicare Levy Surcharge becomes a significant financial factor. A 1.5% tax on a $160,000 salary is $2,400—money that is better off in your pocket or your health fund than with the ATO.

At Tax Falcon, we make the complex simple. By understanding the new 2026 Medicare Levy Surcharge thresholds and using our expert-backed platform, you can lodge your return with the confidence that you’ve managed your health insurance obligations perfectly.

Curious if you’ll be hit with the surcharge this year? Start your 10-minute return with Tax Falcon today and let our experts calculate your best outcome!